The Paystack guide to handling disputes at scale

How we manage chargebacks and fraud claims across multiple markets

In fintech, disputes are inevitable. A customer gets debited twice. A delivery never arrives. A charge appears that they don’t recognize. These moments trigger formal complaints, known as disputes, and how you handle them can make or break customer trust.

Left unmanaged, disputes can lead to revenue loss, reputational damage, and regulatory penalties. But with the right systems in place, they become opportunities: to protect your bottom line, demonstrate operational maturity, and build long-term confidence with both merchants and customers.

In this blog post, we break down how Paystack handles dispute management across multiple markets, from the internal playbooks and tools we use to the frameworks that help us stay compliant and move quickly at scale. Whether you’re starting from scratch or leveling up an existing function, we hope this guide helps you build a dispute operations engine that earns trust and drives resilience.

What counts as a dispute?

A dispute happens when a customer challenges a transaction, usually by contacting their bank, because something about the payment didn’t go as expected. This could be due to a failed delivery, a duplicated charge, or a transaction they simply don’t recognize.

While it might look like a simple customer support issue, a dispute actually sets off a formal process involving several players: the customer’s bank (issuer), the merchant’s bank (acquirer), card networks like Visa or Mastercard, and payment processors like Paystack.

At Paystack, we classify disputes into two main categories:

- Chargebacks: These occur when a customer claims they didn’t receive the value they paid for, or that the product or service was significantly different from what was promised. For example, someone orders a red human hair wig but receives a pink synthetic one.

- Fraud claims: These happen when a customer says they didn’t authorize a transaction, such as a charge resulting from a stolen card or compromised account.

Disputes typically stem from:

- Failed or duplicate transactions

- Unrecognized or unauthorized charges

- Dissatisfaction with a product or service

- Delays or failures in service delivery

Because disputes involve the movement of real money, and can affect both customers and merchants, they’re too important to overlook. If not resolved, disputes can lead to payment reversals (even after delivery), fines from card networks, higher fraud rates that affect the ability to accept payments, and damage to your reputation.

Even if you don’t have a formal dispute team, the process still requires coordination among multiple parties:

- The customer: Initiates the dispute

- The issuer: The customer’s bank

- The acquirer: The merchant’s bank or payment partner

- Card networks (schemes): Visa, Mastercard, and others who enforce rules and timelines

- Other intermediaries: Including fintechs like Paystack and the merchants themselves

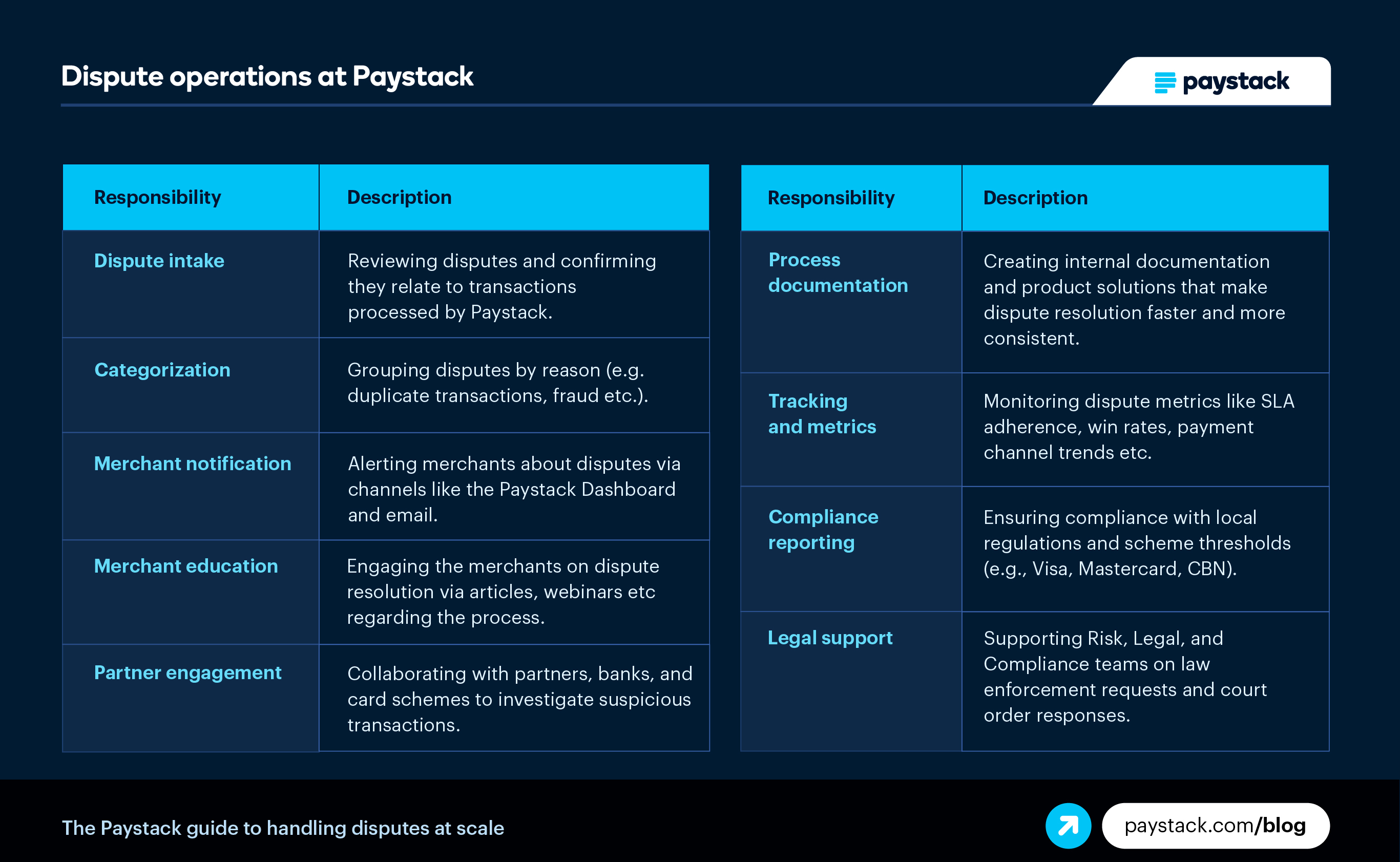

How dispute operations work at Paystack

Disputes don’t resolve themselves, they require fast, coordinated action across multiple teams. At Paystack, the Dispute Operations team is responsible for receiving, investigating, and resolving transaction complaints from banks, card networks, and partners.

We divide this function into two specialist teams:

- Chargeback Operations: Handles disputes where the customer didn’t receive value or the goods/services didn’t meet expectations.

- Fraud Operations: Handles cases where a transaction was unauthorized or reported as fraudulent.

Together, they manage the full dispute lifecycle, from triage to resolution.

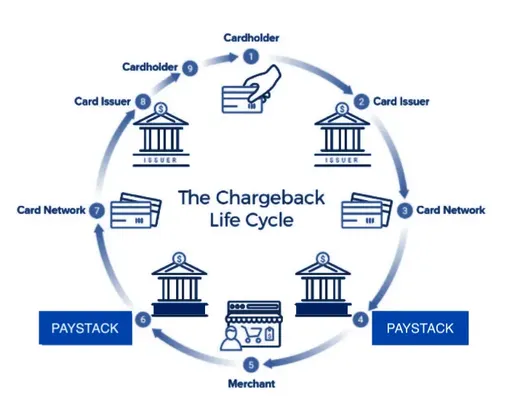

How a dispute moves through our system

We’ve built an end-to-end system that ensures disputes are received, investigated, and resolved efficiently, while keeping everyone informed and compliant.

Here's a step-by-step look at how a dispute moves through our system:

Dispute is logged

A dispute begins when a customer raises a complaint with their bank because either:

- They didn’t receive the product/service they paid for (chargeback), or

- They didn’t authorize the transaction (fraud claim)

The bank then escalates the dispute through email or official channels such as:

- IDRS (Nigeria’s national switch for card payment disputes)

- Arbiter by Interswitch (used for partnership-based disputes across channels like POS)

Disputes are submitted either in bulk (as is common in Nigeria) or individually (as is typical in Ghana, Kenya, and South Africa). All disputes land in our dedicated, CRM-powered inboxes:

We use Front, our CRM platform, to tag, triage, and route disputes to the appropriate team.

Smart categorization and routing

Once received, disputes are reviewed to confirm they relate to Paystack transactions. Valid disputes are then categorized based on:

- Country: Nigeria, Ghana, Kenya, South Africa

- Type: Chargeback or Fraud

- Stage: First chargeback, pre-arbitration, arbitration

- Channel: Cards, POS, Mobile Money, Pay with Transfer

- Source: Bank or card scheme

Each dispute is logged into our internal system and linked to:

- The affected merchant

- Dispute reason and type

- Card scheme reason codes

- Any applicable deductions

- Timeline for response and resolution

Disputes are then assigned to our trained agents who specialize in either Chargeback or Fraud Operations, allowing for quick, accurate handling.

Merchant is notified and equipped to respond

We notify the merchant through their Paystack Dashboard, email, or API. Our communication includes:

- A clear explanation of the dispute reason

- Instructions on what evidence to provide

- The deadline for response (based on the Service Level Agreement)

If a merchant doesn’t respond on time, the dispute is auto-accepted, meaning the customer is refunded and the merchant forfeits the funds.

To support merchants, we also provide:

- Help Center articles

- Instructional videos

- Industry-specific evidence guides

- Periodic webinars on best practices

Service Level Agreement (SLA) management

Disputes are time-sensitive, and missing a deadline can mean automatic losses, where the customer is refunded and the merchant loses the payment.

To avoid this, we manage every dispute against clearly defined timelines, known as Service Level Agreements (SLAs). These SLAs are determined by card scheme rules (like Visa and Mastercard), partner contracts, and local regulations, with regulatory SLAs always taking priority.

At Paystack, we track and act on three key types of SLAs:

- Internal SLAs: How quickly our team must process incoming disputes

- Merchant SLAs: How long merchants have to respond before we take action on their behalf

- Regulatory SLAs: Required response times for legal requests from regulators, law enforcement, or courts

Here’s a quick snapshot of the current dispute SLA timelines across countries:

Once the merchant responds, we review the evidence and prepare a formal response for the card scheme or issuing bank. We make sure that:

- All evidence files are renamed using a standard format (e.g., the transaction reference)

- Responses are submitted within the original email thread for clear traceability

- Bulk disputes are responded to in bulk (where supported) to save time and minimize errors

If everything is in order, we submit the response before the deadline. If not, the case may escalate to the pre-arbitration or arbitration stage, where both the risk and potential costs are significantly higher.

Final feedback and closure

We submit our final response through the appropriate platform, IDRS, Arbiter, or card schemes such as Visa Resolve Online. Based on the outcome:

- If the ruling favors the merchant, the customer is not refunded

- If the ruling favors the customer, the disputed amount is debited from the merchant

In cases involving law enforcement, our Fraud Operations team works closely with the Legal and Risk teams to ensure accuracy and full regulatory compliance.

This structured process enables:

- Fast, consistent intake and triage

- Smart categorization and routing

- Well-informed, empowered merchants

- Strict adherence to SLAs

- Proper documentation and regulatory compliance

A well-run dispute operation not only protects revenue, it builds merchant trust, safeguards your reputation, and ensures you’re always audit-ready.

How to resolve chargebacks

What happens when a customer disputes a payment, and how can you respond to protect your business? Here’s a simple guide to managing chargebacks on your Paystack Dashboard.

Learn how to resolve chargebacks →Essential tools for dispute operations

At Paystack, we combine external industry systems with internal platforms to manage disputes efficiently, reduce manual work, and improve accuracy.

External tools

These are third-party platforms provided by regulators, card schemes, and partners. We use them to receive, manage, and resolve disputes at scale.

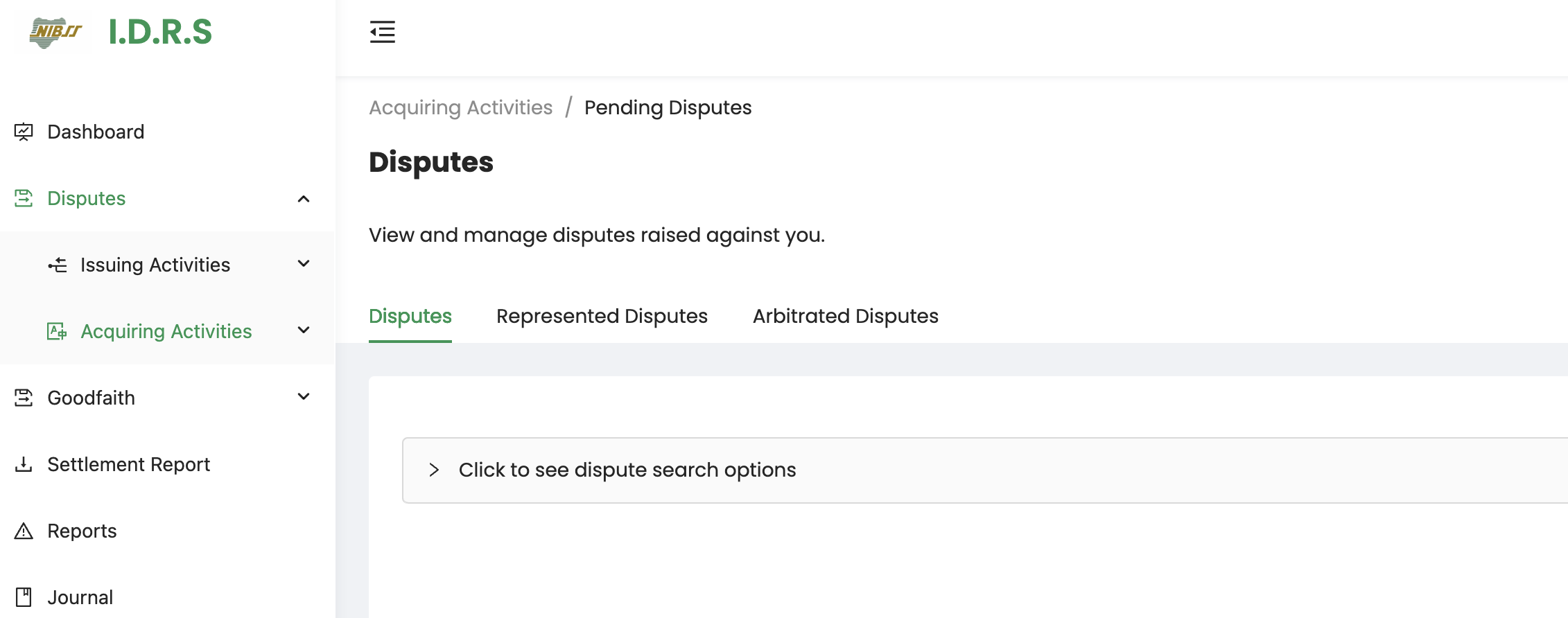

- Industry Dispute Resolution System (IDRS) by NIBSS: Developed by the Central Bank of Nigeria and Nigeria’s central switch, NIBSS (Nigeria Inter-Bank Settlement System), IDRS is the primary platform for managing card payment disputes in Nigeria. It tracks dispute trends, enforces response deadlines, and facilitates post-resolution fund movement. At Paystack, we log in daily to export and respond to incoming cases.

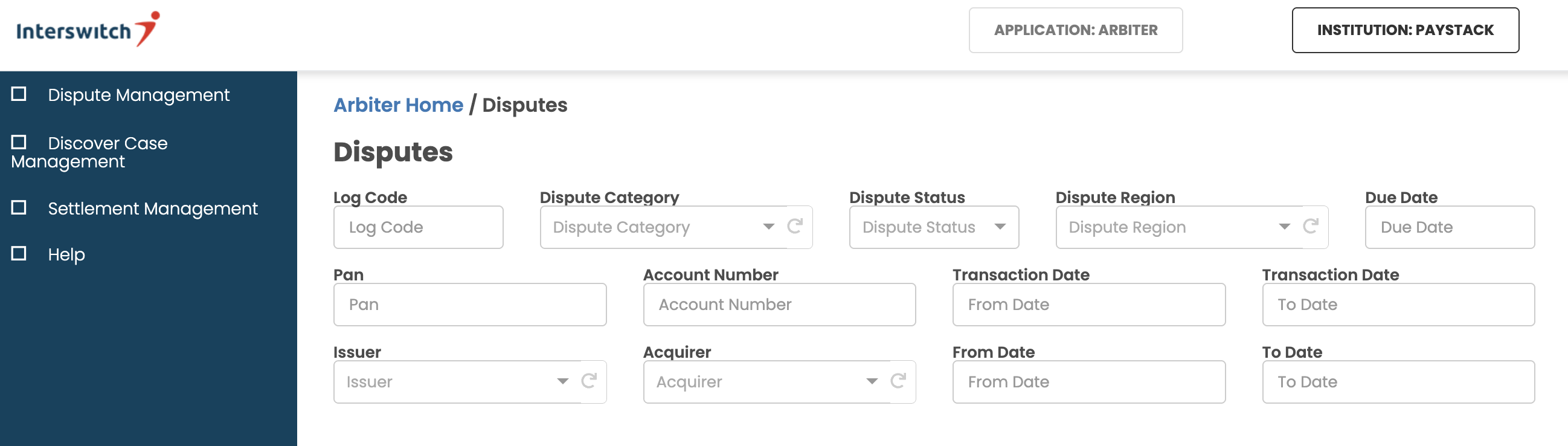

- Arbiter by Interswitch: Arbiter: Arbiter is Interswitch’s dispute resolution platform for POS and other partnership-based channels. Like IDRS, it supports transaction reversals and settlements. It also offers an API that teams can integrate with to manage dispute workflows programmatically.

- Mastercom (Mastercard) and Visa Resolve Online (VROL): These platforms are used by issuers, acquirers, and processors to manage disputes across the Mastercard and Visa networks. They support case filings, representments, and settlement reconciliation. While our acquiring bank previously handled these on our behalf, we now manage most disputes directly through IDRS.

Internal tools

We’ve also built in-house systems to streamline dispute workflows and improve speed, visibility, and control.

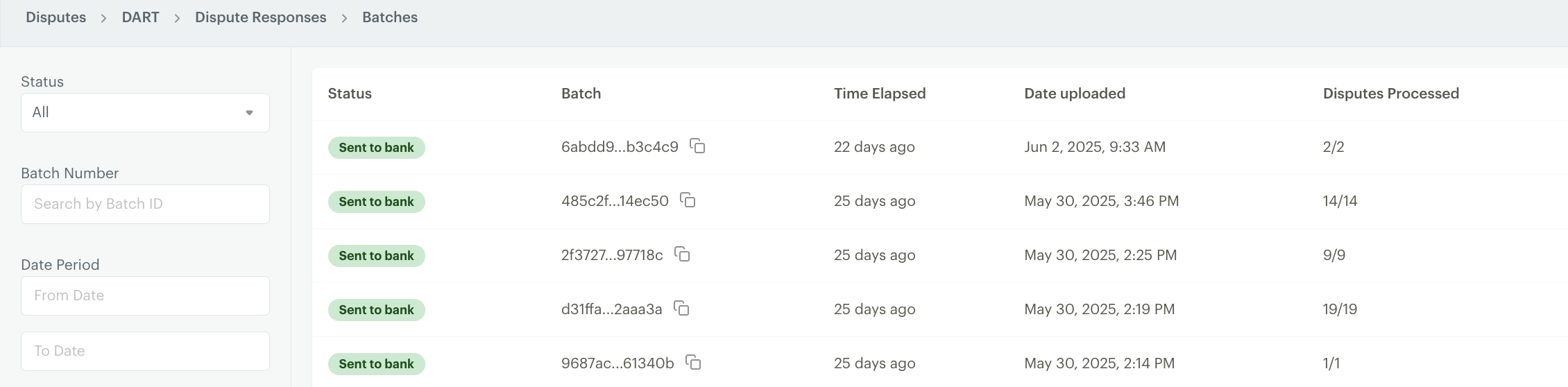

- Dispute Aggregate Resolution Tool (DART): DART is part of our central Watchtower tool. It helps us manage disputes in bulk by:

- Aggregating dispute reports from all partners, no matter the format

- Pushing cases to merchants via the Dashboard and API

- Collecting merchant evidence and responses directly within CRM threads

- Enabling end-to-end tracking and batch review

Thanks to DART, we’ve reduced our turnaround time from almost two hours to under 30 minutes per batch.

- Retool: Retool is a no-code platform we use to build internal tools quickly, without relying on engineering resources. Our Dispute and Data teams co-developed a Retool dashboard to track loss data, with visualizations powered by Metabase. This helps us analyze the reasons behind losses and improve our fraud and risk controls.

- Slack workflow builder: We’ve built custom workflows in Paystack’s Slack to manage incoming requests from other teams. For example, the Support team can request reversals for previously accepted disputes directly within Slack. These requests are logged and tracked for pattern analysis, helping us improve the dispute experience on the Dashboard.

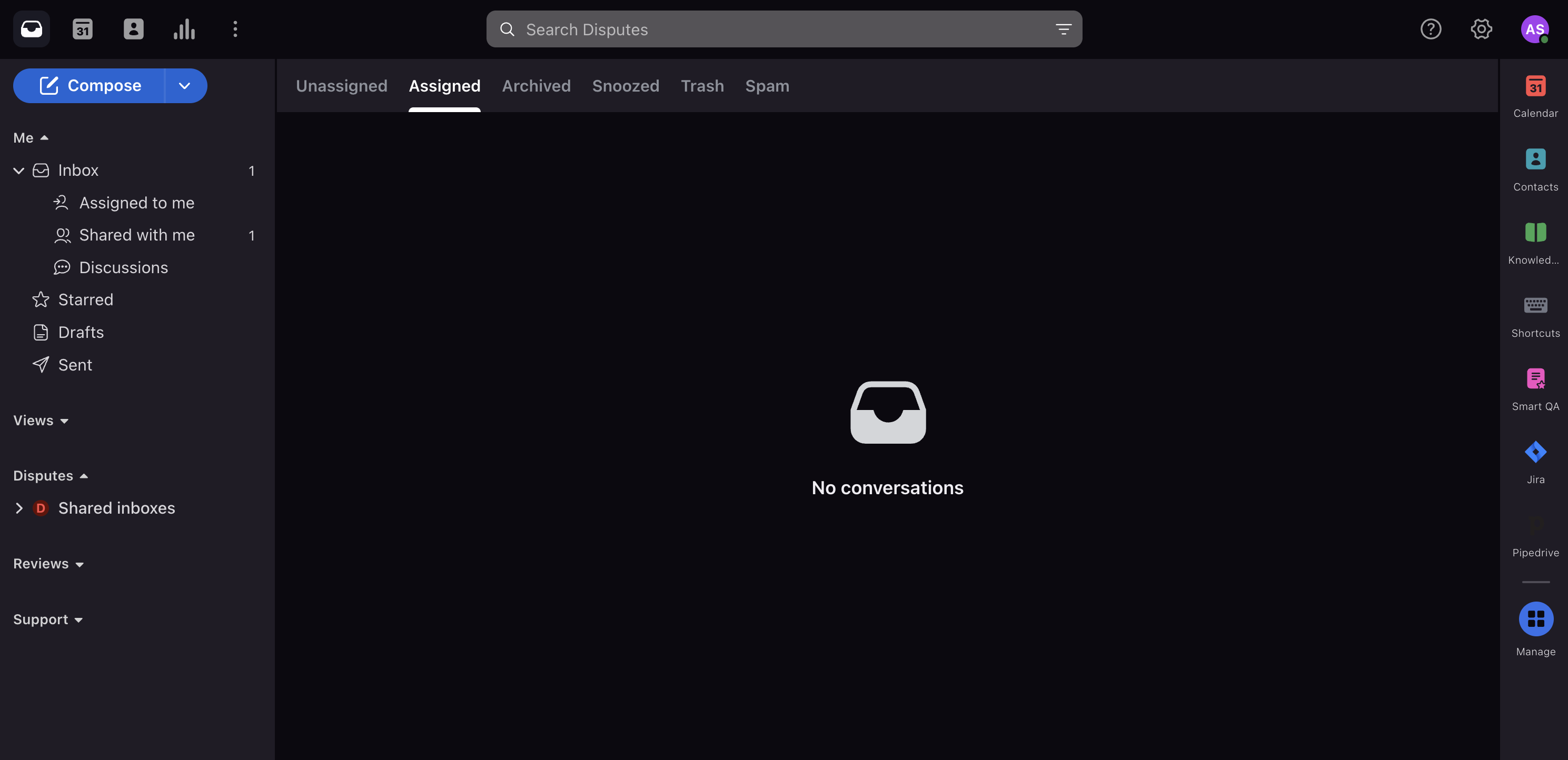

- Front: Front is our CRM platform where we receive inbound dispute reports. We use it to tag cases, assign agents, track SLA performance, and build structured workflows, ensuring that no request falls through the cracks.

Dispute alert system: This internal monitoring system tracks dispute volumes, ratios, and values, both at the merchant level and Paystack-wide. It helps us stay within card scheme thresholds (e.g., Visa’s 0.5%, Mastercard’s 1%).

Merchants nearing these limits are enrolled in the Paystack Remediation Program, which mirrors card scheme remediation policies and helps prevent escalation through proactive education and accountability.

How Paystack helps you manage transaction disputes

Learn how Paystack notifies you about disputes via email, the Dashboard, and webhooks, and how to respond quickly to protect your business.

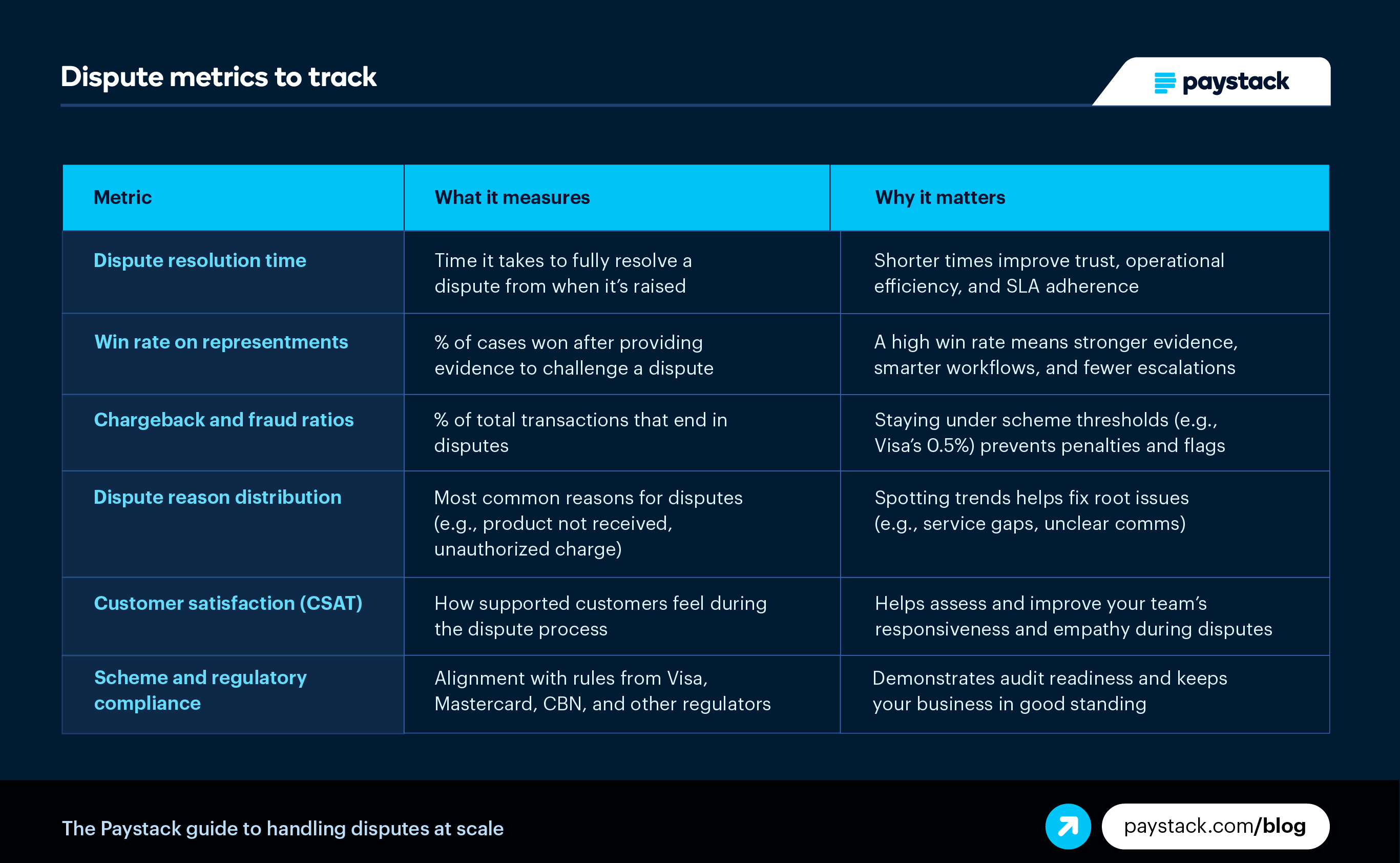

Managing transaction disputes →The metrics we track

We track key metrics to evaluate dispute performance. Doing this helps:

- Catch issues early

- Improve customer and partner trust

- Stay compliant with schemes and regulators

- Continuously improve your operations

Common challenges in dispute operations

Even the most well-designed dispute processes can face friction. Without the right safeguards, challenges like missed deadlines, low win rates, and team burnout can creep in, hurting your reputation with customers, regulators, and partners.

Here are some of the most common pitfalls, and how we manage them at Paystack:

- Volume overwhelm

- The problem: When dispute volumes spike, due to seasonality, fraud surges, or operational bugs, manual processes can’t keep up. This leads to backlogs, missed deadlines, and team burnout.

- How to avoid it: Automate wherever possible. Set up rules to automatically triage low-risk or recurring dispute types. Use templated responses, internal workflows, and batch processing to free up human bandwidth for high-risk cases that need deeper analysis.

- Friendly fraud

- The problem: Not all fraud is malicious. Sometimes, customers dispute valid transactions due to forgetfulness, unclear product descriptions, or even intentional abuse.

- How to avoid it: Train your team to spot patterns of friendly fraud, like repeat disputes from the same user or frequent claims on digital goods. At Paystack, we strengthen our response with service logs, timestamps, and delivery evidence. We also flag high-risk users for further review and monitoring.

- Missing documents

- The problem: You might lose an otherwise winnable case simply because a merchant failed to submit required evidence, or sent it late or in the wrong format.

- How to avoid it: Build a pre-collection system that prompts merchants to upload standard documentation in advance. Provide clear templates, sample evidence, and reminders so merchants know exactly what’s expected. Fast, accurate inputs = higher win rates.

- Bank or partner delays

- The problem: When a dispute requires input from banks, payment processors, or acquiring partners, delays on their side can push you over scheme or regulatory SLAs, exposing your business to penalties or forced reversals.

- How to avoid it: Establish clear escalation paths for time-sensitive handoffs. Document each partner’s SLA expectations, and build internal reminders into your dispute tools or task tracker. Proactive nudges help keep the chain moving and prevent bottlenecks.

How to calculate chargeback and fraud ratios

Tracking dispute metrics like chargeback and fraud ratios helps you spot risks early and protect your business. Learn how to calculate these ratios using your Paystack data, and what your numbers might be telling you.

Calculate fraud and chargeback ratios →Disputes might start as complaints, but they don’t have to end as chaos.

Whether you’re building a dispute operations function from scratch or refining an existing one, the takeaway is clear: don’t wait for volume to overwhelm you before you build for scale. The earlier you invest in smart processes, intuitive tooling, and cross-functional coordination, the more resilient, and trustworthy, your business becomes.

Dispute management may not be the most visible part of your product or business, but it plays a vital role in how your company earns trust and scales sustainably.

If you have questions about how Paystack handles disputes, or you’re a merchant who needs help navigating a chargeback or fraud claim, we’re always happy to help. Send us a note at [email protected].